The book Advances in Nature-Inspired Cyber Security and Resilience is an ambitious but largely speculative collection of academic experiments trying to borrow concepts from biology for cybersecurity. While the underlying resilience principles (adaptivity, diversity, redundancy) are sound, the research remains mostly theoretical and poorly translated to operational use. The algorithms look good in simulation but fail in real environments with real constraints. It’s more a showcase of potential than a set of deployable solutions. Insightful, yes, but still speculative: interesting to read, not ready to run.

A grounded, unromantic review of Nature-Inspired Cyber Security and Resiliency (IET, 2020). The book argues that we can borrow defence principles from biology (immune systems, swarms, self-healing) to build adaptive digital security. The idea is clever but mostly speculative. The theory works on paper; the engineering doesn’t. Nature may be elegant, but enterprise networks aren’t petri dishes. Useful metaphors, immature mechanisms: an interesting academic exercise, not an operational blueprint.

Shockingly the latest report from Forrester Research effectively ends up telling us exactly what we all know already; that the majority of CIOs, CTOs, and other IT leadership and operations management, are not interested in power saving.

In the future, once we’re all ensconced in our virtual reality worlds, is this the way it will all end? On February the 28th, 2009, Tabula Rasa, an MMORPG (like World of Warcraft and RuneScape) was shut down, after failing to attract enough subscribers related to the current economic downturn.

By the afternoon, the West Coast server Hydra was the last server standing. As more and more of its citizenry logged on for the last hurrah, and foreign players from dead servers poured in to squeeze a few more hours out of the game, it became increasingly congested, buggy, and lag-ridden. The intended scenario was indeed playing out not just in the game and the fiction but as a metagame: the active duty population swelled as humanity prepared to make its final stand.

Simon’s description reminded me a little of the recent Doctor Who episode “Utopia”, where at the end of time humanity are huddling together as heat death consumes the planets they had colonised. The ‘Futurekind’ almost like NPCs, also collecting together, prior to being finally terminated.

In a doubly ironic twist of fate, ‘Tabula Rasa’ is Latin for ‘blank slate’, or rather ‘slate wiped clean’, popularised by John Locke as a rather now out of fashion philosophical thesis that individuals are born without any built-in mental content and that their knowledge comes from experience and perception alone (the whole ‘nature’ versus ‘nurture’ debate is more balanced now). It also resembles the off state of the server infrastructure that would have supported the game that presumably had it’s ‘memory’ wiped clean, prior to being redeployed to support other functionality.

After the AGM itself I’ll be doing a presentation called “An Exploration of Cloud Computing” with the following synopsis:

An exploration of Cloud Computing looking at an overview of the subject of and some of the current common definitions available. Looking at the current state of the Cloud Computing market place and Cloud Vendors, what is actually being sold to people. Will also look at the different types of clouds, the differing approaches to engaging with cloud providers, the business models, impact on Business, and how Businesses can exploit the ‘Cloud’.

Answers to key Cloud Computing questions I hope to address include:

What’s Cloud Computing?

What’s different to what we’ve seen before?

What’s driving Cloud Computing adoption?

What types of Cloud are there?

How can I engage with them and use in my Business?

What’s the overview of the Cloud Computing marketplace now?

How is Cloud Computing likely to change?

A number of the members of the Birmingham Committee will be standing down at the AGM so we are looking for volunteers to join the Committee to take part in planning our activities for the 2009-10 session. If you are interested in joining the Committee please contact John Chinn, Branch Secretary, at john.chinn@manchester.ac.uk or you can come forward at the AGM itself.

Details for the event are:

Date: Monday the 18th of May, 2009

Time: AGM at 6pm for 6.30pm, Presentation at 7pm

Location: Trophy Suite, Tally Ho Sports & Conference Centre, Pershore Road, Birmingham B5 7RN

Cost: Free, Presentation open to all (including non-members of BCS), no registration required although we would prefer that you contact the Branch Secretary, John Chinn, at john.chinn@manchester.ac.uk or 0161 306 3733, so that we can advise the caterers of the correct numbers for the buffet.

This Friday I’ll be presenting on the topic of ‘Enterprise Architecture Case Studies’ in Aberystwyth, in an event organised and hosted by the South Wales branch of the BCS.

For more information the event is advertised here with the BCS. The core details are:

Date: 8 May 2009

Time: 17:00 Refreshments / 18:00 Start

Location: The finger buffet is in the foyer of the Computer Science Building and the talk itself will be in Lecture Theatre `A’ in the Physical Sciences Building, both on the Penglais Campus, Aberystwyth University, Aberystwyth.

Cost: Free, open to all (including non-members of the BCS or IET), no registration required.

Here’s what I generally say as an overview of this talk:

The case studies presented explore my experiences with Enterprise Architecture in three major customer engagements. They include an Enterprise Architecture team which led its company into a £70+ million ‘pitfall’; the use of Enterprise Architecture to define a Service Oriented Architecture; and an example of how much Enterprise Architecture is about achieving the proper governance model.

Key takeaways:

Enterprise Architecture best practices drawn from multiple engagements.

How to use good governance to avoid and limit the ‘Ivory Tower’ syndrome.

How to combine Enterprise Architecture and Service Oriented Architecture to deliver sustainable Transformation.

Given the current downturn I’ll also go into some of the issues facing EA programmes due to the credit crunch and what can be done to ensure that they continue to receive executive sponsorship and funding.

Happy to answer any and all questions; please consider that I’ll be attempting to condense three major and very large scale Enterprise Architecture case studies into a talk lasting an hour and a half or so, therefore I will definitely be around to speak with afterwards. ¨C13C

‘Many Thanks’ to Fred Long (of Aberystwyth University) for organising and co-ordinating this event and for Clive King (of Sun) for initially brokering the relationship.

Alan Mather has just released his excellent “Enterprise Architecture in Government” white paper from 2003. This white paper has mythic status in UK Government IT circles because of it’s visionary roadmap of an implementation for Enterprise Architecture (EA) for the UK. Pre-dating the “Cross Government Enterprise Architecture” (XGEA) work of the CTO Council (who hadn’t even been formed at the time, but nor had the CIO Council who commissioned them either) this is the earliest attempt at applying an EA vision to the co-ordination of the UK’s IT and IS portfolio.

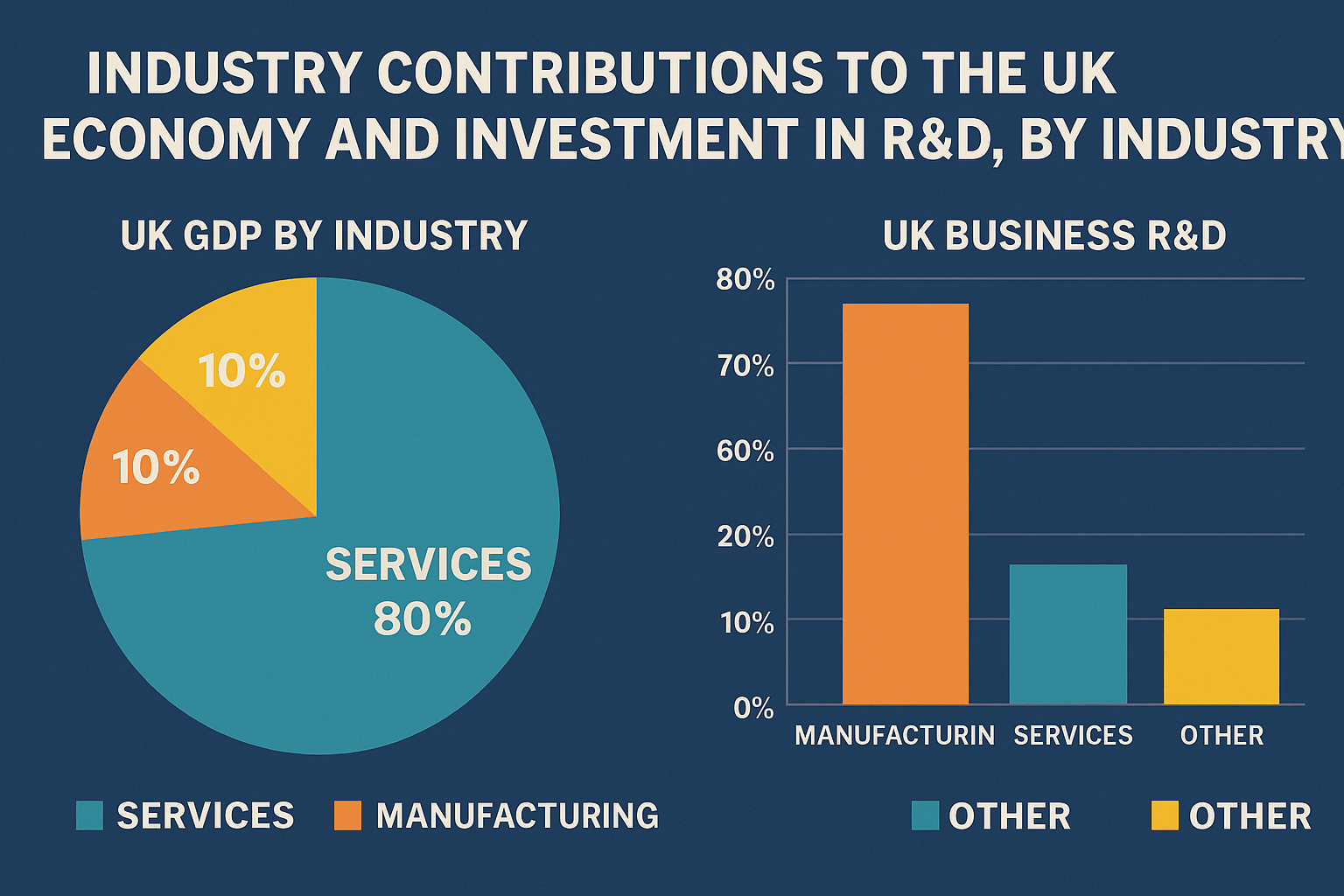

A critical look at the imbalance in the UK economy, highlighting the disproportionate contribution of the services sector to GDP and the overconcentration of R&D investment in manufacturing. It warns that this structural imbalance makes the UK vulnerable to economic shocks and calls for a more diverse and innovation-driven industrial strategy.

Are you concerned about the state of the UK economy in the future, because I know I am, so I’ll be exploring some of the issues being faced by the UK economy, especially when it comes to science, technology, engineering and industry contributions to the UK’s GDP in my next few articles. …..

Kürzlich Philipp Strube meiner ursprünglichen genannten “Cloud Betreuungsmodell” Artikel in seinem Blog-Post “Paas, IAAS, Saas: Den Überblick zu behalten ist wie immer ein Problem für sich”.Recently Philipp Strube mentioned my original ” Cloud Relationship Model ” article in his blog post ” Paas, Iaas, Saas: Den Überblick zu behalten ist wie immer ein Problem für sich “. And given all the traffic it’s generated I thought I’d translate the article into German for Philippe’s readers. Und da der gesamte Verkehr ist es, die ich dachte, ich übersetzen den Artikel in Deutsch für Philippe Leser. I’ve had to use electronic translation (Google, actually) as I’m afraid my written and spoken German isn’t quite good enough to be able to do it manually in a reasonable amount of time. Ich habe die Verwendung elektronischer Übersetzung (Google, eigentlich), wie ich fürchte, mein Wort und Schrift Deutsch ist nicht gut genug sein, um es manuell in einer angemessenen Höhe der Zeit. I haven’t had time to translate the model itself, but you are more than welcome to recreate, reuse and distribute it, although I’d hope you would attribute the original version to me at this site. Ich habe nicht genug Zeit hatte, um das Modell selbst, aber Sie sind mehr als willkommen zu neu, Wiederverwendung und zu verteilen, auch wenn ich hoffe, Sie würden Attribut der ursprünglichen Version für mich auf dieser Seite. Please let me know if there are any outstanding translation issues and I’ll amend them when I can. Bitte lassen Sie mich wissen, wenn es alle noch ausstehenden Fragen und Übersetzung ich ändern, wenn ich kann.

This article was originally a guest post I did recently for Stewart Townsend over at Sun Startup Essentials describing the cloud relationship model I had developed as an artefact when discussing cloud computing. Dieser Artikel war ursprünglich ein Gast-post Ich habe vor kurzem für Stewart Townsend über auf Sonntag Startup Essentials beschreiben die Wolke Modell hatte ich als ein Artefakt bei der Erörterung Wolke Computing.

I wanted a simply model which I could share with people and use as a discussion point, whilst still capturing the major areas of cloud computing which I considered most pertinent. I developed this model about six months ago and have since found it useful when talking with people about cloud computing. Ich wollte ein Modell, das einfach konnte ich mit Menschen und die Verwendung als Diskussion, während die Aufnahme noch die wichtigsten Bereiche der EDV-Wolke, die ich als besonders wichtig. Ich habe dieses Modell an etwa sechs Monaten und haben gefunden, da es für sinnvoll, wenn im Gespräch mit Menschen über Wolke Computing.

Here’s the model and I’ll go though it’s major elements below. Hier ist das Modell, und ich gehe auch wenn es die wichtigsten Elemente aufgeführt.

Major Cloud Communities Major Cloud Gemeinschaften

In the cloud there are three major participants: In den Wolken gibt es im wesentlichen drei Teilnehmer:

the Cloud Providers; building out Clouds, for instance Google, Amazon, etc. Effectively technology providers. die Cloud Provider; Gebäude aus Wolken, zum Beispiel Google, Amazon, etc. effektiv Technologieanbietern.

the Cloud Adopters / Developers; those developing services over the Cloud and some becoming the first generation of Cloud ISVs. I have included Cloud “Service” developers and Cloud ISV developers together. die Wolke Adopters / Entwickler, die Entwicklung von Diensten über den Wolken und einige werden die erste Generation der Cloud ISVs. Ich habe Cloud “Service”-Entwickler und ISV-Cloud Entwickler zusammen. This group are effectively service enablers. Diese Gruppe tatsächlich Dienstfunktionen.

Cloud “End” Users; those using Cloud provisioned services, often without knowing that they are cloud provisioned, the most obvious example of which are the multitude of Facebook users who have no idea there favorite FB app. Cloud “End”-Nutzer, die mit Cloud bereitgestellten Dienstleistungen, oft ohne zu wissen, dass sie Wolken vorhanden, das offensichtlichste Beispiel für die sich die Vielzahl der Facebook-Benutzer, die keine Ahnung haben, es Lieblings-FB App. is running on AWS. läuft auf AWS. These are the service consumers. Es handelt sich um den Dienst der Verbraucher.

I think it’s important to talk about these communities because I keep hearing lots about the Cloud Providers, and even more about the issues and ‘needs’ of the Cloud adopters / developers, but very little in terms of Cloud “End” Users. In a computing eco-system such as this where “services” are supported by and transverse technology providers, service enablers and service consumers an end to end understanding of how this affects these reliant communities is required. Ich denke, es ist wichtig, darüber zu sprechen, weil diese Gemeinschaften ich viel über die Anhörung Cloud-Provider, und noch mehr über die Probleme und Bedürfnisse “der Wolke Anwender / Entwickler, aber nur sehr wenig in Bezug auf die Ableitung von” End “-Benutzer. In einer Eco-Computing-System wie diesem, wo “Dienstleistungen” werden von Quer-und Technologie-Anbietern, Service-Enabler und Service der Verbraucher ein Ende zu Ende zu verstehen, wie sich diese auf dieser Reliant Gemeinden erforderlich ist. Obvious issues such as SLAs for end users and businesses which rely upon high availability and high uptime from there cloud providers come to mind; however other “ilities” and systemic qualities come to mind such as security, and that’s before looking at any detailed breakdown of functional services. Offensichtliche Fragen wie SLAs für Endnutzer und Unternehmen, die sich auf hohe Verfügbarkeit und hohe Verfügbarkeit von dort Wolke Anbieter kommen in den Sinn, aber andere “ilities” und systemischen Eigenschaften kommen in den Sinn wie Sicherheit, und das ist, bevor man eine detaillierte Aufschlüsselung der funktionsfähigen Dienste.

The point here is that the cloud adopters / developers and interestingly the cloud “watchers” (ie the press, media, bloggers and experts) would be mindful to remember the needs and requirements of genuine end users; for myself it’d certainly be invigorating to hear more on this topic area. Der Punkt hier ist, dass die Wolke Anwender / Entwickler und interessanterweise der Wolke “Watchers” (dh der Presse, Medien, Blogger und Experten) würden darauf achten, nicht vergessen, den Bedürfnissen und Anforderungen der Endnutzer echten, für mich würde es sicherlich belebend zu hören, mehr zu diesem Thema werden.

Simon Wardley , a much more eloquent public speaker than myself, does a wonderful pitch which includes a look at the different “as a Service types” which he boils down to being a load of “aaS” (very amusing, and informative, try and catch Simon presenting if you can). Simon Wardley, eine sehr viel beredter Redner als ich, hat eine wunderbare Tonhöhe, die einen Blick auf die verschiedenen “als Service-Typen”, die er läuft darauf hinaus, dass eine Last von “ Aas” (sehr witzig und informativ, versuchen Fang und Simon, die, wenn Sie können).

I wholeheartedly agree that there is a large amount of befuddlement when it comes to the differing “aaS” types and sub-types, and new ones are springing up relatively frequently, however I also think it’s important to not ignore the differences between them. Ich voll und ganz zustimmen, dass es eine große Menge von befuddlement, wenn es darum geht, die unterschiedlichen “ Aas” und Sub-Typen und neue Boden relativ häufig, aber ich denke, es ist wichtig, nicht über die Unterschiede zwischen ihnen.

For me, and many others, I think first popularised by the ” Partly Cloudy – Blue-Sky Thinking About Cloud Computing ” white paper from the 451 Group, the differing “aaS” variants are identified as billing and engagement models. That white paper also postulates the five major Cloud Computing provider models, into which the majority of minor “aaS” variants fall. They are: Für mich und viele andere, ich glaube, von der ersten popularisierte “teilweise bewölkt – Blue-Sky Thinking About Cloud Computing” weißen Papier aus dem 451-Fraktion, die unterschiedlichen “* Aas” Varianten sind als Rechnungs-und Engagement Modelle. Das Weißbuch postuliert auch die fünf größten Anbieter Cloud Computing-Modelle, in denen die Mehrheit der minderjährigen “* Aas” Varianten fallen. Sie sind:

Managed Service Provision (MSP); not only are you hiring your service from the cloud, you’ve someone to run and maintain it too. Managed Service Providing (MSP), nicht nur die Mieten Sie Ihren Service aus der Wolke, die Sie jemandem zu laufen und sie zu pflegen.

Software as a Service (SaaS); pretty much ubiquitous as a term and usually typified by Salesforce.com , who are the SaaS poster child. Software as a Service (SaaS), so ziemlich allgegenwärtig als Begriff und in der Regel gekennzeichnet durch Salesforce.com, wer sind die SaaS-Poster Kind.

Platform as a Service (PaaS); the application platform most commonly associated with Amazon Web Services. Platform as a Service (Paas); die Anwendung Plattform am häufigsten im Zusammenhang mit Amazon Web Services.

Infrastructure as a Service (IaaS); Infrastructure as a Service (IAAS);

Major Architectural Layers Major Architectural Ebenen

Also included in the diagram are the major architectural layers that are included in each of the above billing / engagement models offered by the Cloud providers. Auch in der Grafik sind die wichtigsten architektonischen Schichten, die in jedem der oben genannten Billing / Engagement Modelle von der Cloud-Anbieter. They are: Sie sind:

Operations; and this really is operations supporting functional business processes, rather than supporting the technology itself. Operations, und das ist wirklich funktionellen Maßnahmen zur Förderung von Geschäftsprozessen, sondern als Unterstützung der Technologie.

Service layer; made up of application code, bespoke code, high-level ISV offerings. Service-Schicht, aus der Anwendung Code, maßgeschneiderten Code, High-Level-ISV-Angebote.

Platform layer; made up of standard platform software ie app. Plattform Schicht; aus der Standard-Plattform-Software, dh App. servers, DB servers, web servers, etc., and an example implementation would be a LAMP stack. Server, DB-Server, Web-Server, usw., und ein Beispiel dafür wäre eine LAMP-Stack.

Infrastructure layer; made up of (i) infrastructure software (ievirtualisation and OS software), (ii) the hardware platform and server infrastructure, and (iii) the storage platform. Infrastruktur-Schicht, die sich aus (i) Infrastruktur-Software (ievirtualisation und OS-Software), (ii) die Hardware-Plattform-und Server-Infrastruktur und (iii) die Speicherplattform.

Network layer; made up of routers, firewalls, gateways, and other network technology. Network Layer; aus Routern, Firewalls, Gateways und andere Netzwerk-Technologie.

This rather oversimplifies the architecture, as it’s important to note that each of the cloud billing / engagement models use capabilities from each of the above architectural layers; for instance their can be a lot of service simply in managing a network, however these describe the major architectural components (which support the service being procured), not simply ancillary functions, effectively what are the cloud providers customers principally paying for. Diese eher übermäßige der Architektur, wie es ist wichtig zu beachten, dass jeder der Wolke Abrechnung / Engagement Modelle verwenden Fähigkeiten aus jedem der oben genannten architektonischen Schichten, zum Beispiel ihre kann eine Menge Service einfach in die Verwaltung eines Netzes, aber diese Beschreibung der wichtigsten Architektur-Komponenten (die Unterstützung der Service werden soll), nicht einfach Nebendienstleistungen Funktionen, wirksam sind, was die Wolke Anbieter hauptsächlich Kunden bezahlen.

Delta of Effort / Delta of Opportunity Delta Aufwand / Delta von Opportunity

This is much more than the ‘gap’ between the cloud providers and the cloud users, wherein the cloud adopters / developers sit, the gap between the cloud providers and the end cloud users can be called the delta of effort, but also the delta of opportunity. Dies ist viel mehr als die “Lücke” zwischen der Wolke und den Wolken Benutzer, dass die Wolke Anwender / Entwickler sitzen, die Kluft zwischen der Wolke und den Ende Wolke Benutzer kann die Delta-Aufwand, sondern auch das Delta der Chance. ¨C88C

It is the delta of effort in terms of skills, abilities, experience and technology that the cloud adopter needs to deliver a functional service to their own “End Users”. This will be potentially a major area of cost to the cloud adopters. Es ist das Delta der Anstrengungen im Hinblick auf die Fertigkeiten, Fähigkeiten, Erfahrungen und Technologien, dass die Wolke Anwender braucht, um eine funktionale Service für ihre eigenen “End User”. Dies ist möglicherweise ein wichtiger Bereich der Kosten für die Wolke adopters. But it’s also the delta of opportunity;in terms of ‘room’ to innovate. Aber es ist auch das Delta der Möglichkeit, im Hinblick auf die “Zimmer”, zu innovieren.

The more capability procured from the cloud provider (ie higher up the stack as a whole), the less you have to do (and procure) yourself. However the less procured from the cloud provider the more opportunity you have engineer a differentiating technology stack yourself. This itself has it’s disadvantages because the cloud adopters / developers could potentially not realise the true and best value of their cloud providers infrastructure. Die Fähigkeit, die aus der Wolke-Anbieter (z. B. die weiter oben in der Stack als Ganzes), desto weniger müssen Sie tun (und Beschaffung) selber. Doch die weniger die aus der Wolke Anbieter die Möglichkeit haben Sie ein Ingenieur differirende Technologie-Stack selbst . Dieses selbst hat seine Nachteile, weil die Wolke Anwender / Entwickler möglicherweise nicht, die wahre und beste Wert ihrer Wolke Anbieter Infrastruktur.

I suspect that there is an optimum level, around the Platform Layer, which abstracts enough complexity away (ie you don’t have to procure servers, networks, implementation or technology operations staff), but also leaves enough room to innovate and produce software engineered value. Arguably the only current successful cloud provider, based upon market share, perception, revenue and customer take up, is Amazon Web Services (AWS) who provide a PaaS offering. Ich vermute, dass es ein optimales Niveau, um die Plattform-Layer, die Abstracts genug Komplexität entfernt (dh Sie müssen nicht beschaffen Servern, Netzwerken, der Durchführung oder der Technologie Operationen Mitarbeiter), aber auch genügend Spielraum für Innovation und Herstellung von Software-Engineering Wert. die wohl nur die aktuellen erfolgreiche Anbieter Wolke, die sich auf Marktanteil, Wahrnehmung, Einnahmen und Kunden nehmen, ist Amazon Web Services (AWS), die eine Paas bieten.

Summary Zusammenfassung

Hope you enjoyed the article, in summary if developing cloud services or even building out a cloud infrastructure I would recommend that you focus on your users and if your a cloud provider, your users’ users; remembering that only a certain percentage of those users will be customers (I won’t getting into discussing Chris Anderson’s 5% recommended conversion rate for the long tail , however I would recommend understanding what some of those calculations might be). Hoffen, dass Ihnen die Artikel, in der Zusammenfassung, wenn die Entwicklung Wolke oder sogar Ausbau der Infrastruktur eine Wolke Ich würde empfehlen, dass Sie sich auf Ihre Benutzer und wenn Ihr Provider eine Wolke, die Benutzer “Benutzer; Erinnerung, dass nur ein bestimmter Prozentsatz der Nutzer Kunden werden (ich werde nicht immer in der Diskussion Chris Anderson, 5% empfohlen, Conversion-Rate für den langen Schwanz, aber ich würde empfehlen, zu verstehen, was einige dieser Berechnungen werden könnten).

If you’re looking to develop services over the cloud, think carefully about where you and your teams skills lie, and where would you most want them focusing there efforts; working on installing and tuning operating systems and application platforms or writing business value focused applications and services, before choosing at which level to engage with your cloud provider(s). Wenn Sie zur Entwicklung von Diensten über den Wolken, sich genau überlegen, wo Sie und Ihre Teams Fähigkeiten liegen, und wo würden Sie am meisten wollen, dass sie sich es Bemühungen, auf die Installation und Tuning-Betriebssysteme und Plattformen Antrag schriftlich oder geschäftlichen Nutzen sich Anwendungen und Dienstleistungen, vor der Wahl, auf welcher Ebene, sich mit Ihrem Provider Wolke (n).

I haven’t mentioned enterprise adoption of cloud based services, and that’s because I’d like to post that in the near future in a different article. Ich habe nicht erwähnt Unternehmen Annahme Wolke Dienste, und dass deshalb, weil ich möchte, dass die Post in der nahen Zukunft in einem anderen Artikel.

Hope you enjoyed the article and all the best, Hoffen, dass Ihnen die Artikel und alles Gute,

Simon Wardley, Software Services Manager at Canonical UK and noted Cloud Computing expert and public speaker, responds to my article “Cloud Relationship Model“, with specific mention of my paraphrasing of a talk I saw him give; and thereby explains the history behind the “*aaS” double entendre.

Seriously though, the number of heads on the “*aaS” Hydra continues to grow, and Simon’s comment soon focuses upon the genuine need for a stable and standardised taxonomy, something I agree with wholeheartedly, along with a little bit of temperance and cool-headedness when it comes to thinking up and announcing more “*aaS” classifications…

Back in early 2007 when I gave a talk at ETECH, I described the changes in the industry as a continued shift of the computing stack from a product to a service based economy.

At that time I often categorised the computing stack into three layers – software, software platform and hardware (back from 2006). Whilst I had made comments that the software layer was really about applications and therefore SaaS should have had a more unfortunate acronym, this was not my true crime nor the origin of the joke.

The problem was that whilst SaaS and HaaS had been in common usage, the mid layer was known as SaaS Platform. This neither fitted neatly into the naming convention nor was it correct, as this layer of the stack contained many framework elements. So I started to describe this as the framework layer and FaaS seemed to be the obvious choice.

Hence at OSCON in Jul’07 I described the stack as a trio of SaaS, FaaS and HaaS.

Robert Lefkowitz (in a later talk at OSCON’07) warned us that this trio of “oh so wrong” nomenclature would lead to a whole lot of “aaS” and hence the joke was born.

Well Robert, as always, was spot on. In the last few years we’ve seen a plethora of different “aaS” terms (at last count it was about 16, including multiple versions of DaaS). The last few years has seen a constant exercise in revisionism.

Whilst the distinction between the layers of the computing stack is valid and meaningful, especially in context of the shift from products to services, what is not meaningful is the constant creation and recreation of terms.

Fortunately we now seem to be settling down to a three layer stack of application, platform and infrastructure – though I’m sure there is going to be more arguments.

This is why I argue the one thing we need in cloud computing today is a stable taxonomy.

I’ve recently updated my site to use Disqus the blog comment hosting and conversation site.

Done this for two reasons:

Firstly my usually frustration with any status quo means I want more functionality delivered yesterday, and although I’d started to have a look at the functionality I wanted and how I might add it as a Roller macro / velocity code I didn’t want to spend a huge amount of time coding it out (the functionality I specifically wanted was the separation of comments and trackbacks, as well as comment ‘threads’).

Secondly to gain readership and comments from the sizeable blog comment audience that Disqus have built up (Disqus is estimated to be running on over 30,000+ servers).

I’ve already had a couple of comments from Disqus members, and I’ll have to see how it goes before I start heralding it as an unprecedented success, but I’m very pleased with the results (both aesthetic and functional).

Sadly the Disqus comment import function was initially provided for WordPress and Blogger, but apparently wasn’t fully functional; subsequently an update is due out soon that will hopefully include Roller Weblogger. See this Disqus forum entry, and it’s threads for more info: How do I import comments?

Given this was the case I wanted to make sure my blog supported my new Disqus commenting system, but would still show my old comments if there where any for an entry. Here are a few examples:

The code I developed, which has to be separated into two components (number of comments associated with a blog entry, and comment entry form and comment display), is below, but if you use or copy it please note that you need to replace the Disqus supplied JavaScript for my site with your Disqus comments hosted sites JavaScript code. ¨C18C

Combined Roller Weblogger and Disqus Number of Comments code

For comment numbers I’ve broken it down into displaying “n Comments” for Disqus on it’s own, whilst “x Comments (new, via Disqus) and y Comments (legacy, via Roller)” for comments hosted on both systems.

This replaces the code in the Roller Weblogger “_day” template which displays the number of comments per blog entry.

Don’t forget to replace occurrences of ‘eclectic’, my blog handle, with yours (just one, about the fifth line from the end).

## Number of Comments

<a href="$url.entry($entry.anchor)#disqus_thread">View Comments</a>

#set($commentCount = $entry.commentCount)

#if ($commentCount > 0)

(new, via <a href="https://web.archive.org/web/20090830081824/https://www.disqus.com/" target="_blank">Disqus</a>) and

#if ($commentCount == 1)

<a href="$url.comments($entry.anchor)">$commentCount Comment</a> (old, via <a href="https://web.archive.org/web/20090830081824/https://rollerweblogger.org/" target="_blank">Roller</a>)

#else

<a href="$url.comments($entry.anchor)">$commentCount Comments</a> (old, via <a href="https://web.archive.org/web/20090830081824/https://rollerweblogger.org/" target="_blank">Roller</a>)

#end

#end

<script type="text/javascript">

//<[CDATA[

(function() {

var links = document.getElementsByTagName('a');

var query = '?';

for(var i = 0; i < links.length; i++) {

if(links[i].href.indexOf('#disqus_thread') >= 0) {

query += 'url' + i + '=' + encodeURIComponent(links[i].href) + '&';

}

}

document.write('<script type="text/javascript" src="https://web.archive.org/web/20090830081824/https://disqus.com/forums/eclectic/get_num_replies.js' + query + '"></' + 'script>');

})();

//]]>

</script>

Combined Roller Weblogger and Disqus Comment entry and Comments display code

This basically displays the Disqus commenting system, along with any Disqus hosted comments, however if any ‘legacy’ Roller Weblogger hosted comments are found it displays those too.

It replaces the code in the Roller Weblogger “permalink” template which displays comments themselves (the same changes may need to be made to the “weblog” and “searchresults” templates too).

## Comments

<h2>Comments (new, via <a href="https://web.archive.org/web/20090830081824/https://www.disqus.com/" target="_blank">Disqus</a>)</h2>

<div id="disqus_thread"></div><script type="text/javascript" src="https://web.archive.org/web/20090830081824js_/https://disqus.com/forums/eclectic/embed.js"></script><noscript><a href="https://web.archive.org/web/20090830081824/https://eclectic.disqus.com/?url=ref">View the forum thread.</a></noscript><a href="https://web.archive.org/web/20090830081824/https://disqus.com/" class="dsq-brlink">blog comments powered by <span class="logo-disqus">Disqus</span></a>

##showWeblogEntryComments($model.weblogEntry)

##showWeblogEntryCommentForm($model.weblogEntry)

<br></br>

#set($commentCount = $entry.commentCount)

#if ($commentCount > 0)

<h2>Comments (old, via <a href="https://web.archive.org/web/20090830081824/https://rollerweblogger.org/" target="_blank">Roller</a>)</h2>

#showWeblogEntryComments($model.weblogEntry)

<br></br>

#end

Additional benefits that I’ve picked up by implementing Disqus include:

Following commentators.

Having my, and my sites, comments followed.

Being able to easily ‘reblog’ my comments and make blog entries out of them (looking forward to trying this, although I haven’t yet).