A critical look at the imbalance in the UK economy, highlighting the disproportionate contribution of the services sector to GDP and the overconcentration of R&D investment in manufacturing. It warns that this structural imbalance makes the UK vulnerable to economic shocks and calls for a more diverse and innovation-driven industrial strategy.

My biggest concern about the UK economy is in two very related areas, firstly the imbalance of industry contributions to UK GDP, and secondly the imbalance of investment in innovation in those industries.

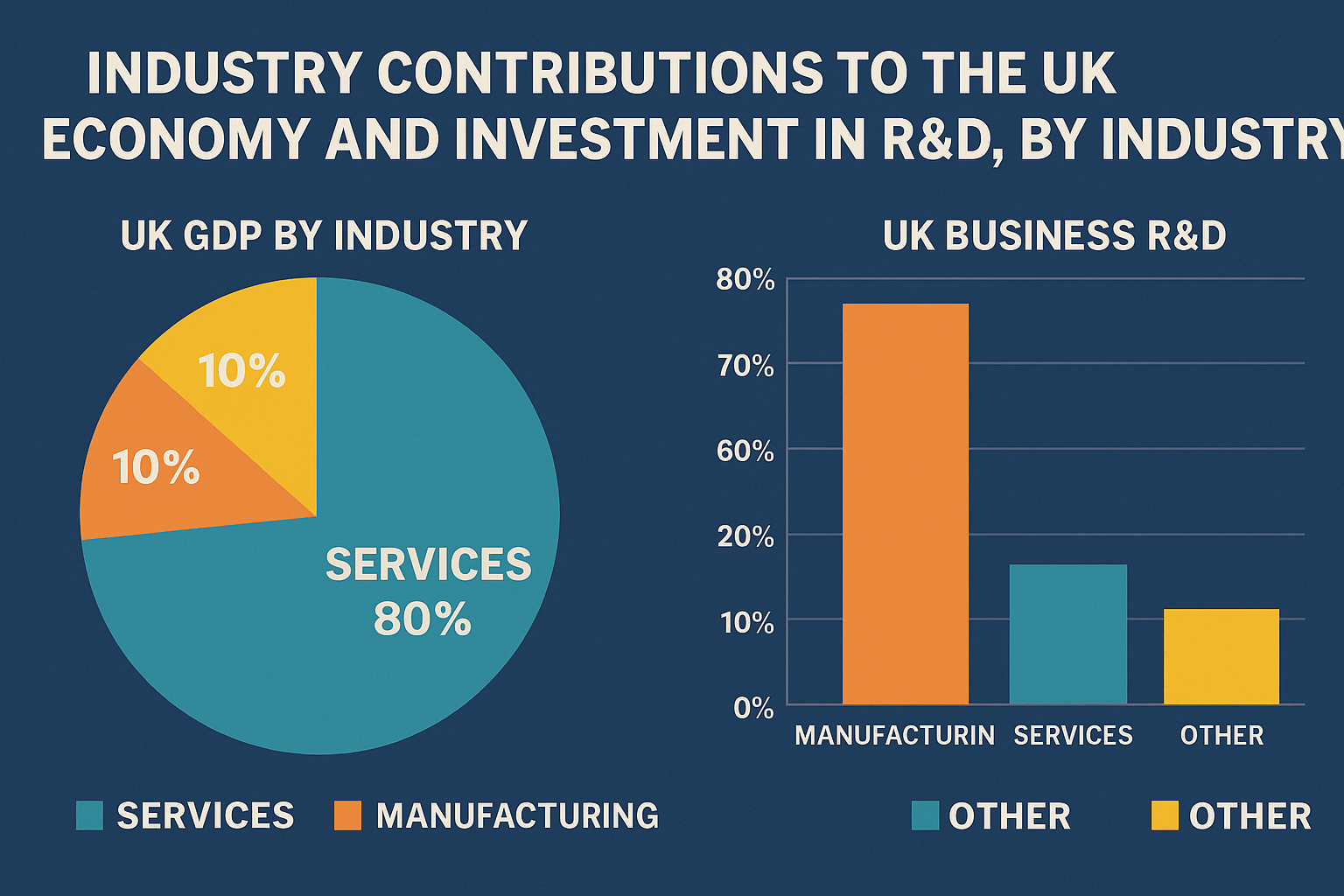

When I speak about the imbalance of industry contributions to UK GDP I’m actually talking about which industry sectors are contributing to the UK GDP.

Over the last few years the GDP of the UK has been around £1.2 to £1.3 Trillion (where 1 Trillion equates to 1,000 Billion); this is traditionally circa $2.35 Trillion for those of you who prefer dollar notation.

If we break down GDP contributions as percentages the most obvious point to be made is that Services makes up the majority at over 75% of the GDP contribution to the UK economy (and up until the credit crunch circa 40% of GDP contribution were from Financial Services alone). Manufacturing as an industry sector currently supports just 13% of the UK GDP (as a comparison the USA is circa 19% and Germany is circa 23%) and the actual amount is around £150 Billion. The rest is made up of Agriculture (hovering at 1% and just below) and ‘other’ Industry.

It occurs to me that frankly this isn’t a particularly balanced model; especially when it comes to global recessions such as the one we find our selves in now which, because of our dependence on single industry sectors, affects us so adversely. And nor is it particularly self sustaining.

I’m not alone in thinking this, Warren Buffet warned long ago that the UK’s over reliance on it’s service sector exposed the economy to a higher risk of recession, and George Soros has recently been quoted in the UK press that his concern about the recovery of the UK economy is it’s dependence on the financial services industry.

Sir John Rose, Chief Executive of Rolls-Royce, and one of the UK’s most inspiring business leaders, is vocal about the UK’s need to balance it’s industries contribution to it’s GDP, he has this to say on the subject:

“This country needs a broad portfolio of assets.” adding “There is an over dependence on financial services. If you are a one-trick pony, you have to hope that people continue to like your trick. If they stop liking it, you become pet food.” and “…the credit crisis gives a unique opportunity to start answering questions about how this country should be earning its living in the 21st century.”

You may agree or disagree, or perhaps you’d be interested in what the spread and distribution of UK GDP contributions from differing Industries should or could be, something I believe needs a certain amount of consideration and planning, something you’d imagine would be in the UK’s “Industrial Strategy”, which according to key experts, sadly, does not exist as a coherent and authoritative source. What is key to me is that we collectively recognise the imbalance and look at what it means and what our options might be, including attempting to encourage or stimulate other areas of the economy where appropriate.

All of this brings me to the second, related area, and probably the one that I find more worrying as I increasingly think about the future of the UK economy; that is the imbalance of investment in innovation across the industry sectors in the UK.

Circa 75% of all UK business Research and Development is in Manufacturing alone. Let me restate that another way to bring the point clearer. 75% of all investment in R&D;, innovation and future offerings is done in a single industry sector which contributes just 13% of the economy. Genuinely this worries me a great deal, because therefore, 87% of the economy (which is not manufacturing, and is predominantly services) is contributing just 25% of the entire amount being invested in the future. Yes that’s right, nearly 90% of the UK economy will be dependant on a quarter of the total investment in innovation. This does not look like a good investment on the future state of the economy to me. Nor does it give me a warm and fuzzy feeling when it comes to the future of non-manufacturing businesses either, and lets be clear here, the future of the service industry.

These two points could be playing off against each other of course, in that industry contributions to the economy need to be rebalanced, possibly with a larger (or even, much larger) contribution from manufacturing. And that subsequently the imbalance in terms of investment in R&D; across industry could possibly be less of a worry than I currently imagine.

However I really don’t expect for manufacturing to make up 75% of the GDP contribution anywhere in the future, and I’m still very concerned about the lack of investment in R&D; in the Services industry of the UK. I’d really like better awareness of the issue as a whole, and perhaps go so far to look for more focused stimulation from Government to encourage investment in R&D; in the Services sector.

Recently the CBI’s Innovation, Science and Technology (IST) committee have been working on a number of upcoming white papers, and I have been vocal in having the above issues brought to light in those. Thankfully I got a great of support from the other members of the IST, especially those who are working in the Services sector. I’ll let you know when the white papers I’ve mentioned are available from the CBI web site.

So in a nutshell what am I saying? Firstly let’s investigate and hopefully work towards a more balanced, recession proof economy, with a bigger contribution from high value and “just in time” manufacturing, if it is viable, and secondly let’s see more investment in R&D;, innovation and the future from the Services industry. To achieve any of this we’ll need significant support from Government departments like DBERR and DIUS, followed by the Treasury, to act as sponsors, and finally some Government assistance, whether that be legislation, stimulation, or something softer (the current favourite doing the rounds across the political parties is that of the ‘nudge’ as exemplified by Richard Thaler and Cass R. Sunstein, in their book “Nudge: Improving Decisions About Health, Wealth, and Happiness”).

Please Note: All data in this piece comes from these sources, in this order, the Economist ‘Pocket World in Figures (2009 Edition)’, the Economist magazine, the CBI, the IoD, and the BBC. Furthermore, despite manufacturing making up 13% of the UK economy, the UK is still the sixth largest manufacturer in the World (although there are some very big gaps between the economic output of the top five and the UK, and so I may very well touch on the state of the UK manufacturing industry in the future).

Links for this article:

- Recovered link: https://horkan.com/2009/05/05/uk-economy-gdp-contribution-imbalance

- Archived link: https://web.archive.org/web/20100715125601/https://blogs.sun.com/eclectic/entry/uk_economy_gdp_contribution_imbalance

- Original link:

https://blogs.sun.com/eclectic/entry/uk_economy_gdp_contribution_imbalance