CYBERUK 2026 signals a shift from building a cyber ecosystem to operating a national cyber system. Across a series of analyses, a consistent pattern emerges: policy is coherent, execution is demanding, and outcomes are uneven. This article draws those strands together to show that the gap between strategy and delivery is not incidental; it is structural, and it defines how the system behaves.

Executive Summary

CYBERUK 2026 marks a transition point in UK cyber strategy.

Over the past decade, the focus has been on building the components of a national cyber ecosystem: institutions, baseline standards, and a capable private sector. That phase has reached maturity. What now emerges is a shift towards operating that system under real-world conditions.

Across this analysis series, examining both the Security Minister’s speech and the NCSC CEO’s keynote, a consistent picture becomes clear.

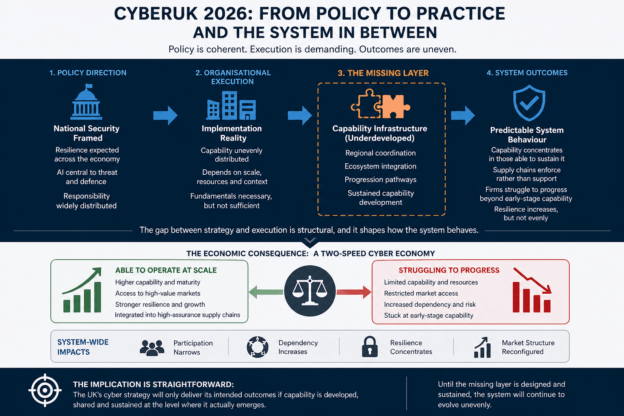

At the policy level, the direction is coherent. Cyber security is framed as a matter of national security, resilience is expected across the economy, and artificial intelligence is positioned as central to both the evolving threat landscape and its defence.

At the implementation level, however, capability is unevenly distributed. The ability to deliver resilience is shaped by organisational scale, resources, and context. Fundamentals remain necessary, but increasingly depend on sustained capability, integration, and operational maturity.

Taken together, this produces a system that does not fail but behaves in predictable ways.

Capability concentrates in organisations able to sustain it.

Supply chains shift from support mechanisms to enforcement mechanisms.

Firms enter the system, but many struggle to progress beyond early-stage capability.

Resilience increases, but does not distribute evenly across the economy.

The result is the emergence of a two-speed cyber economy, in which cyber security is no longer solely a technical control, but increasingly a condition of participation in higher-value markets.

CSRB-style policy will squeeze SMEs out of higher-value markets unless capability is actively supported at both the policy and firm levels.

Without deliberate capability infrastructure, SMEs will be structurally excluded, and this is a design problem, not a performance problem.

The final element of the analysis identifies the underlying cause of this dynamic.

Between national strategy and organisational execution lies a layer that remains underdeveloped: the capability infrastructure through which resilience is actually built and sustained. This includes regional coordination, ecosystem integration, and the mechanisms that enable firms to move from early-stage activity to scalable delivery.

Where this layer is present, capability compounds. Where it is absent, it stalls.

In practice, this shapes not only security outcomes, but market structure, determining which organisations are able to participate, scale, and remain within the system over time.

The implication is straightforward.

The UK has defined its cyber strategy with increasing clarity. But the ability to deliver that strategy depends on whether capability can be developed and distributed at the level where it actually emerges.

Until that layer is explicitly designed, coordinated, and sustained, the system will continue to evolve unevenly, reflecting not a failure of intent but the constraints of the current delivery structure.

Contents

1. Introduction: From Description to Operation

CYBERUK 2026 marked a clear shift in the UK’s cyber security posture.

Across the keynote speeches from the Security Minister and the NCSC CEO, a coherent direction emerged:

- cyber security is now firmly embedded as national security

- resilience is expected across the entire economy

- AI is central to both threat and defence

- responsibility is being distributed beyond specialist teams

Taken at face value, this is a story of maturity.

The UK has moved from building a cyber ecosystem to beginning to operate a cyber system.

But that transition introduces a more complex reality.

1.1 The CYBERUK 2026 Analysis Series

This article forms part five of a five-part analysis of CYBERUK 2026, examining the UK’s evolving cyber strategy from policy through to operational reality and system-level implications:

- CYBERUK 2026: From Policy Ecosystem to Operational Doctrine

Dan Jarvis MBE, UK Security Minister’s, CYBERUK 2026 speech, signals the shift from ecosystem-building to operating a national cyber system - CYBERUK 2026: The Perfect Storm and the Limits of Fundamentals

NCSC CEO Richard Horne’s CYBERUK 2026 keynote discusses the operational reality of cyber security under technological and geopolitical pressure - CYBERUK 2026: System Ambition vs Operational Reality and the Rise of a Two-Speed Cyber Economy

The structural tension between policy ambition and uneven organisational capability - CYBERUK 2026: The Missing Layer Between Strategy and Execution is Regional Capability Infrastructure

The capability infrastructure required to translate the national strategy into distributed resilience - CYBERUK 2026: From Policy to Practice and the System in Between

A synthesis of these perspectives, examining what they imply for how the system behaves in practice and what it means to be able to deliver it

Taken together, these pieces move from:

intent → execution → consequence → constraint → implication

2. What the Analysis Reveals

Across the preceding analyses, covering policy direction, operational reality, system-level tension, and the layer required to connect them, a consistent insight emerges:

The UK’s cyber strategy is coherent in design, but in practice it is producing uneven resilience, because capability is not being built and distributed at the level where it is required.

For the past decade, UK cyber strategy has focused on building:

- institutions

- baseline standards

- a competitive sector

That work is largely complete.

What CYBERUK 2026 signals is a shift from:

describing the system → attempting to operate it

This is a fundamentally different challenge.

Because systems do not operate through structure alone.

They operate through:

- capability

- coordination

- and the interaction between actors under real conditions

3. From Gap to Behaviour

The existence of a gap between strategy and delivery is not, in itself, surprising.

What matters is what that gap produces.

Where capability is assumed rather than systematically built and distributed, the system behaves in predictable ways:

- capability concentrates in organisations with scale, capital, and existing maturity

- supply chains become enforcement mechanisms rather than support structures

- smaller organisations struggle not just with security, but with progression

- resilience becomes unevenly distributed across the economy

These are not unintended side effects.

They are the natural consequences of how the system is structured.

4. A System That Evolves Unevenly

The emerging picture is not of a system that fails.

It is a system that:

- operates

- adapts

- but does so unevenly

So firms enter the ecosystem but struggle to progress beyond early-stage capability, failing to move from initial activity to sustained, scalable delivery, something reflected in many stimulation programmes, where only a small number of initiatives continue once funding ends.

The direction of travel is clear:

- higher standards

- stronger enforcement

- deeper integration of AI

- closer coupling between government and industry

But the outcome is not uniform.

A system built on uneven capability produces uneven resilience.

This leads to a bifurcation:

- organisations that can operate securely at scale

- organisations that struggle to move beyond baseline capability

And increasingly:

cyber security becomes a condition of market access.

5. From Technical Challenge to Economic Structure

At this point, the nature of the issue changes.

This is no longer solely a question of cyber security practice.

It becomes a question of:

- market structure

- participation

- and economic distribution

Because if access to markets depends on:

- continuous assurance

- demonstrable resilience

- integration into high-assurance supply chains

Then the ability to meet those requirements determines:

who participates, and who does not

In practice, this reshapes the system.

In effect, this functions as a form of industrial structuring, shaping which firms are able to participate, scale, and remain within the market.

So:

- Capability concentrates

- Participation narrows

- Dependency increases

And critically:

progression through the system becomes constrained, not by entry, but by the ability to sustain capability over time.

6. Looking Beyond CYBERUK

The dynamics described here are not unique to CYBERUK 2026.

They reflect deeper patterns in how cyber capability develops across the UK, particularly in how firms:

- enter the market

- attempt to scale

- and sustain themselves over time

Some of these patterns are explored in more detail in the analysis of regional cyber ecosystems and firm lifecycle dynamics.

Evidence from regional cyber ecosystems shows that, without coordination and sustained support, firms tend to cluster in the early stages rather than progressing to scalable, market-facing capabilities.

It emerges through:

- local industrial context

- access to networks and coordination

- and sustained interaction between industry, academia, and government

Where those conditions exist, capability compounds.

In practice, capability does not simply emerge from access to standards or funding. It progresses from early-stage activity to commercial adoption and then to scalable delivery, something many firms struggle to achieve without sustained support.

Where they do not, it stalls.

This is why capability is not simply a function of investment or intent.

It is a function of:

environment, coordination, and progression pathways

7. Why This Matters Now

The UK is at a point of transition.

The system is no longer being designed, it is being used.

And as it is used:

- pressures increase

- expectations rise

- and structural imbalances become visible

If capability cannot be distributed effectively:

- resilience will concentrate

- participation will narrow

- and the system will evolve unevenly

Not because the strategy is wrong:

but because the mechanisms required to deliver it are incomplete.

8. Conclusion

CYBERUK 2026 shows that the UK has moved decisively into a new phase of cyber strategy.

The focus is no longer on building the ecosystem.

It is about operating the system.

The preceding analysis identified a missing layer between strategy and execution: the capability infrastructure required to translate national policy into distributed resilience.

The question is not whether that layer exists.

It is what its absence means.

A system designed at national level will only succeed if it can be delivered where capability is actually built.

This pattern is already visible in how cyber capability develops across different parts of the UK economy.

Until that layer is explicitly designed, coordinated, and sustained, the system will not fail, but it will evolve unevenly, concentrating capability, narrowing participation, and reshaping the market in ways that are not yet fully acknowledged.

That is not a failure of policy direction.

It is a consequence of how the system is being delivered.